This has been Buiter's view all along:

"Can the US economy afford a Keynesian stimulus?

January 5, 2009

Economic policy is based on a collection of half-truths. The nature of these half-truths changes occasionally. Economics as a scholarly discipline consists in the periodic rediscovery and refinement of old half-truths. Little progress has been made in the past century or so towards understanding how economic policy, rules, legislation and regulation influence economic fluctuations, financial stability, growth, poverty or inequality. We know that a few extreme approaches that have been tried yield lousy results - central planning, self-regulating financial markets - but we don’t know much that is constructive beyond that.( I AGREE )

The main uses of economics as a scholarly discipline are therefore negative or destructive - pointing out that certain things don’t make sense and won’t deliver the promised results. This blog post falls into that category.

Much bad policy advice derives from a misunderstanding of the short-run and long-run impacts of events and policies. Too often for comfort I hear variations on the following statements: “the long run is just a sequence of short runs, so if we make sure things always make sense in the short run, the long run will take care of itself.” This fallacy, which I shall, unfairly, label the Keynesian fallacy, compounds three errors.

The first error is( 1 ) the leap from the correct assertion that a long interval of time is the sum of successive short intervals of time to the incorrect impact that the long-run impact of a policy or event is in any sense the sum of its short-run impacts. The second error is( 2 ) the failure to recognise that our models (formal or implicit) of how the economy works are inevitably incomplete( TRUE ). Parts of the transmission mechanism - positive or negative feedbacks and other causal links between actions today, future outcomes and anticipations today of future outcomes and future actions - that can safely be ignored when we consider the impact of a policy over a year or two can come back to haunt us with a vengeance over a three-year or longer horizon. The third error is that, ( 3 ) when economic agents, households, firms, portfolio managers and asset market prices are even in part forward-looking, the long run is now. More precisely, the long-run consequences of current policies can, through private sector expectations ( YES )and through forward-looking asset prices influence consumption behaviour, employment and investment decisions and asset prices today( TRUE ).

Matching the Keynesian fallacy is the view that just because a certain set of policies is not sustainable, in the sense that it cannot be maintained indefinitely, such policies should not be implemented even temporarily. I will call this the sustainability fallacy. It rests on the simple error that identifies a sustainable policy rule or programme, with a specific constant policy action. A sustainable, sensible or even optimal contingent policy programme, or contingent sequence of policy actions, will in general involve specific actions that will be undone, reversed or even neutralised by later contingent policy actions in the opposite direction. These specific actions may be eminently sensible, even from a long-run perspective, provided they are not maintained indefinitely and are, and are expected to be, reversed in due course, according to the rule, when the state of the economy has evolved or when a new unexpected contingency arises.

US fiscal policy: the Keynesian fallacy on steroids

How does this apply to the macroeconomic stabilisation policy and the financial stability support policies being pursued in the US today?

First, the fiscal policy actions pursued thus far by the Bush administration, but even more so the policy proposals leaked by Obama’s proto-administration are afflicted by the Keynesian fallacy on steroids. They appear to exist outside time, with neither the long-run consequences of the actions like to be implemented over the next couple of years, nor the history that brought the US to its current predicament, the initial conditions, being given any serious attention.

A nation in fundamental disequilibrium: the disappearance of American ‘alpha’

Even before the crisis erupted, around the middle of 2007, the US economy was in fundamental disequilibrium. The external primary deficit (the external current account deficit plus US net foreign investment income) was running at around five or six percent of GDP. The US was also a net external debtor( SPENDER COUNTRY ), Its net external investment position (at fair value, or the statisticians best guess at it) was somewhere between minus 20 percent and minus 30 percent of annual GDP. The US economy managed to finance this debt and deficit position quite comfortably because it gave foreigners an atrocious rate of return on their investment in the US - a rate of return much lower, when expressed in a common currency, than the rate of return earned by US-resident investors abroad.

Some of this lousy ex-post average return on foreign investment in the US was no doubt unexpected and one-off. If risk premia on foreign investment in the US and on US investment abroad were the same, the appearance of excess returns to US investment abroad relative to foreign investment in the US may simply have been an example of the ‘peso problem’ - a ‘small-sample bias’ in expected returns. Assume expected returns are equal using the true distribution of returns. The true distribution may, however, have fat or long tails, with extreme negative values that occur infrequently (e.g. the collapse of a currency peg). The term ‘peso problem’ came from observations on realised returns on US dollar-denominated securities and Mexican peso-denominated securities during the 1970s. The forward premium on the Mexican peso relative to the US dollar was positive through 22 years of a pegged exchange rate, until August 1976, of eight Mexican pesos to the US dollar. On September 1, 1976, the peso devalued by 45 percent vis-à-vis the US dollar.

The term peso problem was, according to Paul Krugman, invented by a bunch of MIT graduate students of the late Rudi Dornbusch. William S. Krasker published the first paper using the expression (”The ‘peso problem’ in testing the efficiency of forward exchange markets”, Journal of Monetary Economics, Volume 6, Issue 2, April 1980, pages 269-276), long before fat tails, black swans and related regurgitations of the same phenomenon became current. The attribution of the expression ‘peso problem’ to Milton Friedman is almost certainly incorrect.

When the disaster scenario (a collapse of the currency peg) materialises, the roof caves in for peso investments. Before the collapse, statisticians, unlike market participants, don’t know the true distribution but base their calculation of the expected return on a sample during which the extreme event has not (yet) materialised. The result is that statisticians overestimate the expected return on the peso (there has been no depreciation of the peso during my sample, therefore the future expected depreciation rate is zero) and attribute the positive (risk-adjusted) rate of return differential on the peso to ‘alpha’. It is, of course, ‘false alpha, as the September 1, 1976 collapse of the peso (repeated a number of times since then) made clear.

Some of the excess returns on US investment abroad relative to foreign investment in the US, may have been anticipated, and may have reflected a low or even a negative risk-premium on US investment. In that case, if risk-adjusted rates of return to foreign investment in the US and on US investment abroad are the same, we would expect that the so far unrealised risk will in due course materialise and blow a large hole in the US external asset position( YIKES ). Even with a very long enough sample, ex-post realised average rates of return on investing in the US will still be lower than ex-post realised rates of return on investment abroad, but the (ex-post) positive correlation between the return on foreign investment and consumption growth could be stronger for foreign investment in the US than for US investment abroad.

Some of the excess returns on US investment abroad relative to foreign investment in the US may have reflected true alpha, that is, true US alpha - excess risk-adjusted returns on investment in the US, permitting the US to offer lower financial pecuniary risk-adjusted rates of return, because, somehow, the US offered foreign investors unique liquidity, security and safety( YES ). Because of its unique position as the world’s largest economy, the world’s one remaining military and political superpower (since the demise of the Soviet Union in 1991) and the world’s joint-leading financial centre (with the City of London), the US could offer foreign investors lousy US returns on their investments in the US, without causing them to take their money and run( YES. THAT'S HOW IMPORTANT GUARANTEES ARE. ). This is the ‘dark matter’ explanation proposed by Hausmann and Sturzenegger for the ‘alpha’ earned by the US on its (negative) net foreign investment position ....

Now, from H and S:

"In short, the US is a net provider of knowledge, liquidity and insurance( GOVERMENT GUARANTEES. YOU KNOW HOW IMPORTANT THAT THIS IS IN MY OPINION. ). As the world became more global financially, the increasing asset value of these services underlies the spectacular increase in dark matter over the last two decades."

Back to Buiter:

" If such was the case (a doubtful proposition at best, in my view), that time is definitely gone. The past eight years of imperial overstretch, hubris and domestic and international abuse of power on the part of the Bush administration has left the US materially weakened financially, economically, politically and morally ( TRUE ). Even the most hard-nosed, Guantanamo-bay-indifferent potential foreign investor in the US must recognise that its financial system has collapsed. Key wholesale markets are frozen; the internationally active part of its financial system has either been nationalised or underwritten and guaranteed by the Federal government in other ways( TRUE ). Most market-mediated financial intermediation has ground to a halt, and the Fed is desperately trying to replace private markets and financial institutions to intermediate between households and non-financial operations. The problem is not confined to commercial banks, investment banks and universal banks. It extends to insurance companies (AIG), Quangos (a British term meaning Quasi-Autonomous Government Organisations) like Fannie Mae and Freddie Mac, amorphous entities like GEC and GMac and many others. ( TRUE )

The legal framework for the regulation of financial markets and institutions is a complete shambles. Even given the dismal state of the legal framework, the actual performance of key regulators like the Fed and the SEC has been appalling, with astonishing examples of incompetence and regulatory capture.( FRAUD, ETC. )

There is no chance that a nation as reputationally scarred and maimed as the US is today, could extract any true ‘alpha’ from foreign investors for the next 25 years or so. So the US will have to start to pay a normal market price for the net resources it borrows from abroad. It will therefore have to start to generate primary surpluses, on average, for the indefinite future. A nation with credibility as regards its commitment to meeting its obligations could afford to delay the onset of the period of pain. It could borrow more from abroad today, because foreign creditors and investors are confident that, in due course, the country would be willing and able to generate the (correspondingly larger) future primary external surpluses required to service its external obligations. I don’t believe the US has either the external credibility or the goodwill capital any longer to ask, Oliver Twist-like, for a little more leeway, a little more latitude. I believe that markets - both the private players and the large public players managing the foreign exchange reserves of the PRC, Hong Kong, Taiwan, Singapore, the Gulf states, Japan and other nations - will make this clear. ( HERE I DISAGREE. THE SAVER COUNTRIES ARE TEMPTED, FOR SOCIAL STABILITY REASONS, TO TRY AND KEEP THE SAVER COUNTRY/SPENDER COUNTRY SYMBIOSIS GOING. )

There will, before long (my best guess is between 2 and 5 years from now) be a global dumping of US dollar assets, including US government assets. Old habits die hard( IT CAN LEAD TO SOCIAL DISLOCATIONS ). The US dollar and US Treasury Bills and Bonds are still viewed as a safe haven by many( TRUE ). But learning takes place. The notion that the US Federal government will be able to generate the primary surpluses required to service its debt without selling much of it to the Fed on a permanent basis, or that the nation as a whole will be able to generate the primary surpluses to service the negative net foreign investment position without the benefit of ‘dark matter’ or ‘American alpha’ is not credible. ( PROBABLY TRUE )

So two things will have to happen, on average and for the indefinite future, going forward. First, there will have to be some combination of higher taxes as a share of GDP or lower non-interest public spending as a share of GDP( I AGREE ). Second, there will have to be a large increase in national saving relative to domestic capital formation. ( GRADUALLY, YES )

The need for a massive resource transfer towards the public sector

As regards the required massive transfer of resources from the public to the private sector in the US, it has long been recognised by those who look at long-term prospects for taxes and public spending in the US, that a combined permanent increase in the tax share/reduction in the share of public spending in GDP of around ten percentage points would be required to fund existing Medicare and Medicaid commitments (and to a lesser extent Social Security commitments). In the past decade the US has legislated for its citizens (though Medicare, Medicaid and Social Security retirement) a West-European-style welfare state( TRUE ). Obama’s proposals for universal health care will complete this process. The US has done so with a general government public expenditure share in GDP that is about 10 percentage points below the West-European average (in the mid-thirties for the US, in the mid-forties in for Western Europe. Evolving demographics and entitlement will drive US welfare state expenditure towards the West-European levels, in the absence of political decisions in the US to limit coverage and entitlements( TRUE ).

This resource shift from the private to the public sector would only manifest itself gradually however, and no doubt, there will be changes in (whittling down of) these commitments before their full impact is felt. ( I AGREE )

The US Federal government has taken on massive additional contingent liabilities through its bail out/underwriting( GUARANTEES ) of the US financial system (and possibly other bits of the US economic system that are too politically( TRUE ) connected to fail). Together will the foreseeable increase in actual Federal government liabilities because of vastly increased future Federal deficits, this implies the need for a future private to public sector resource transfer that is most unlikely to be politically feasible without recourse to inflation( A BAD CHOICE ). The only alternative is default on the Federal debt( I SAY THAT SAVER COUNTRIES MIGHT GO FOR THIS. ). There is little doubt, in my view, that the Federal authorities will choose the inflation and currency depreciation route over the default route.

If I can figure this out, so can anyone in the US or abroad who follows recent economic developments. The dawning of the realisation( INFLATION ) will lead to the dumping of the assets.( BECAUSE THEY WILL BE WORTH LESS IF HELD. AN INFLATION RUN. )

Even if the US Federal government decides to go the inflation route for ‘paying off’ public debt is would be too politically difficult to service through tax increases or spending cuts, it is unlikely that some, not insignificant, resource transfer from the private to the public sector will have to take place. And there we have the short run-long run conundrum. If the economy were at full employment and a high rate of capacity utilisation today, it would still require a permanent resource transfer from the private sector to the public sector, that is, higher taxes or lower public spending. But for cyclical purposes( OUR CURRENT RECESSION ), lower taxes and higher public spending are indicated - provided the authorities have the credibility to commit themselves to future tax increases and/or spending cuts that would not just take care of the existing obligation, but also of the additional debt that would be incurred as a result of the Keynesian stimulus.( I'M FOR THIS SOLUTION. )

The latest gurgling about the magnitude of the Obama fiscal stimulus are certainly impressive: $775 bn or so (around five percent of GDP) over two years. This on top of a Federal deficit that even absent these stimuli could easily top $750 bn. I now anticipate a Federal deficit of between $1.5 trillion and $2.0 trillion for 2009 and something slightly lower for $ 2010. With both the Fed and the Treasury exposed to trillions of private assets and institutions of doubtful quality and solvency, the stock of US Federal debt could easily increase by many more trillions of US dollars during the next couple of years.

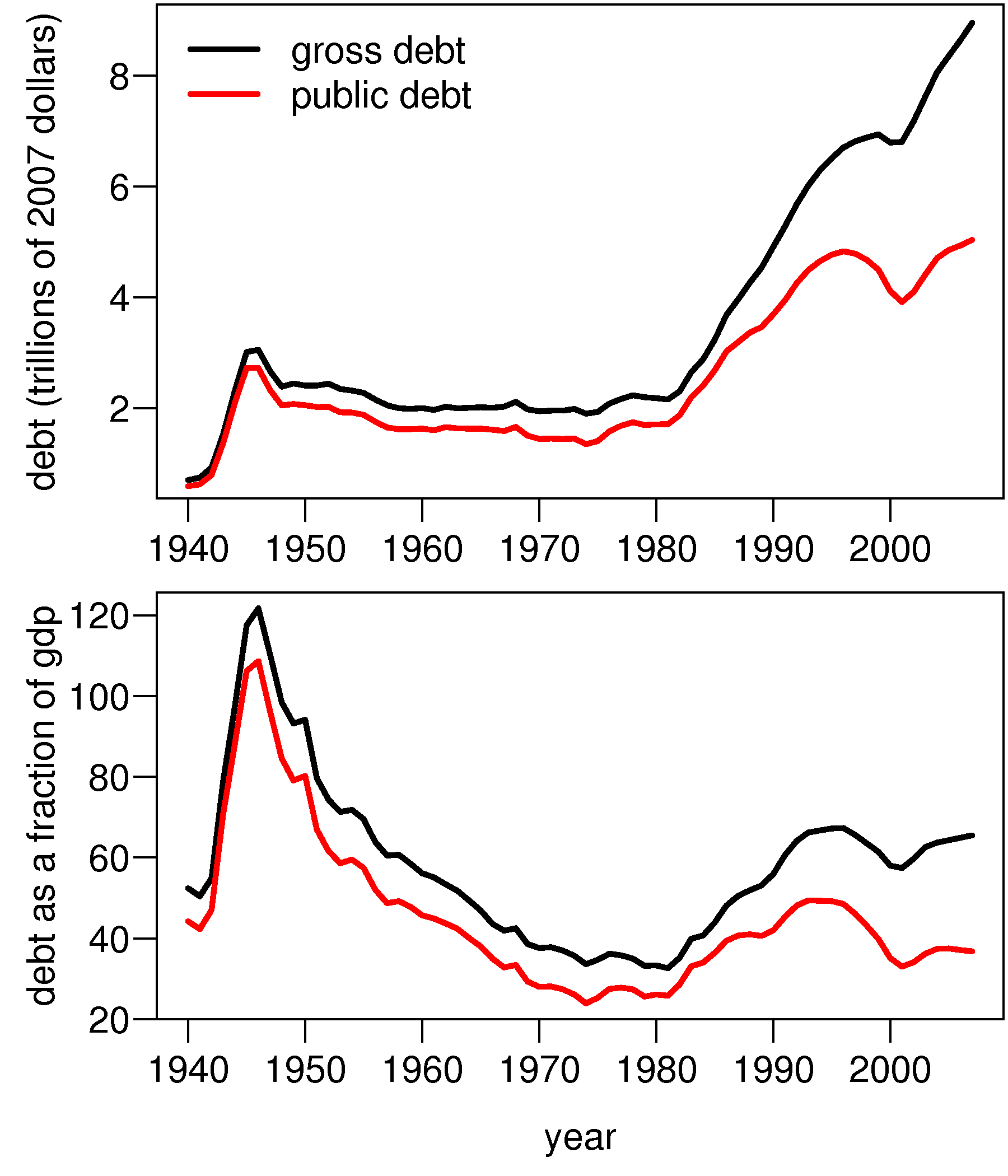

Those familiar with the post World War I and post-World War II public debt levels will not be impressed with even a doubling of the public (Federal) debt held by the public as share of GDP, from its current level of around 40 percent of annual GDP (gross public debt, including debt held by other government agencies, like the Social Security Trust Fund, stands at around 70 percent of GDP). Chart 1 is taken from Wikepedia. Following World War II public debt stood at more than 100 percent of annual GDP.

Chart 1

usdebt.png

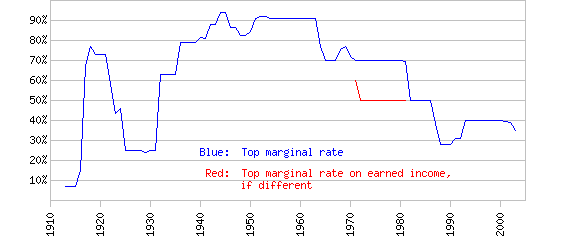

A simple (coarse?) indicator of ‘tax tolerance’ - willingness to pay taxes or to make others pay taxes( YES ) - is the highest marginal rate of personal income tax. For the US this is shown in Table 2 below. It is taken from the website of TruthAndPolitics.org.

Chart 2

That, however, was then. The debt was incurred to finance a temporary bulge in public spending motivated by a shared cause: defeating Japan and the Nazis. The current debt is the result of the irresponsibility, profligacy and incompetence of some( FRAUD, ETC. ). Achieving a political consensus to raise taxes or cut spending to restore US government solvency is going to test even the talents of that Great Communicator, Barack Obama.

If you add to the Keynesian fiscal stimulus package Obama’s ambitions for increasing infrastructure investment to stimulate growth, to fund (not quite) universal healthcare and to stimulate alternative energy production and use, the incompatibility of US public spending ambitions and the political capacity to raise the necessary revenues is glaring. So the government would borrow. From whom? Not from the domestic private sector. They are saving rather little and are being discourage from saving what little they are saving by the fiscal stimulus package. So the US government will borrow abroad to finance its infrastructure, health ambitions and green agenda? Some day perhaps. But not during Obama’s presidency.

So will the Keynesian demand stimulus work? For a while ( a couple of years, say) it may. When the consequences for the public debt of both the Keynesian stimulus and the realisation of the losses from the assets and commitments the Fed and the Treasury have taken onto their balance sheets become apparent, the demand stimulus will fade and may be reserved as precautionary( A PROACTIVITY RUN ) behaviour takes over in the private sector. My recommendation is to go easy on the fiscal stimulus( I AGREE ). The US government is ill-placed financially and fiscally, to engage in short-term fiscal heroics. All they can really do is pray for a stronger-than-expected revival of global demand, without any major stimulus from the US.

The need for a massive resource transfer towards the rest of the world

Beggars can’t be choosers. The US has been able to get away with decades of private sector improvidence because of two unique and time-limited factors. The first is a sequence of capital gains on household assets (stocks and real estate) that provided a lovely substitute( TRUE ) for saving to provide for retirement, old age and a rainy day. The second was the excess returns earned by the US on its net foreign investment (its ability to borrow at an unbelievably low rate of interest/rate of return, because of the unique position of the US as the ultimate source of liquidity and security( GUARANTEES ).

Both rational drivers of a low US saving rate are gone. The US housing market and global stock markets have imploded. It will take years, even decades, to restore household financial wealth-income ratios to levels that don’t guarantee retirement in poverty for much of the US population. The rest of the world will also no longer lend to the US at a negative nominal (and real) interest rate, as it has done for years.( AGAIN, I'M NOT SO SURE. )

So the US has to shift aggregate demand from domestic demand to external demand. And it has to shift production from non-tradables to tradables - exportable and import-competing goods and services. By how much? At full employment, probably at least six and more likely by around eight percent of GDP.

As regards shifting production towards tradables, this will not be easy( NO IT WON'T ). And policy is pushing in the wrong direction. The Bushbama administrations have decided to bail out the US car industry( FOR SOCIAL REASONS ). That industry does not produce cars the rest of the world wants. If and when the global economy recovers and oil prices rise to $150 per barrel again, US consumers also won’t want the cars produced by Detroit. Sure they can change. They could have changed in 1973, in 1980 and at any time since then. If they could change, they probably would have by now.

Other US industries are more competitive internationally. But shifting resources towards tradables and away from non-tradables will require re-training and re-education as well as a significant depreciation of the US dollar’s real exchange rate - which amounts to a significant cut in real wages( FOREIGN GOODS WILL BECOME MORE EXPENSIVE ). Chart 3, which shows the US broad real effective exchange rate index, provided by the Fed, shows the behaviour of one measure of the real exchange rate since 1973.

Chart 3

In the past year, the effective real exchange rate of the US dollar has in fact strengthened rather than weakened, thus impeding the necessary external adjustment. With the short risk-free nominal interest rate effectively at the zero floor, conventional expansionary monetary policy cannot be used any longer to weaken the exchange rate. The effect of quantitative easing and qualitative easing on the exchange rate are ambiguous. If they succeed in stimulating spending by credit-constrained businesses and households, it could well strengthen the currency and weaken the trade balance.

In the decades since I first lived in the US, the quality of secondary education and of vocational training appears to have worsened. Despite the excellence of some institutions, including the wide range and variety of community colleges that give a second chance to so many Americans, the educational system of the US increasingly resembles that of the UK: islands of excellence in a sea of mediocrity. This means that, to become competitive, if you cannot compete on quality and innovation, you will have to compete on price. A larger real exchange rate depreciation and cut in real consumer wages will be required to achieve a given shift of resources to the external sector.

With all the talk about investing in the future, improving infrastructure and creating a dynamic competitive economy, I don’t think the Obama administration will want to achieve the necessary shift of resources towards the rest of the world by reducing domestic investment. In fact, in the one area where domestic investment could and should be reduced (residential construction), there is bipartisan support for boosting investment in residential housing( REALLY ? ). That leaves an increase in national saving as the only way to achieve the required primary external surplus. The government is, however, planning to boost its spending and cut taxes. No increase in public saving therefore can be anticipated for many years( A FEW YEARS ) to come.

The private sector in the US is, at last, saving. We have gone from a declining growth rate of private consumption to a declining level of private consumption. But what do the policy authorities do? Rising household saving equals falling household consumption equals declining effective demand equals longer and deeper recession. Can’t have that. Here is a tax cut. If you can no longer borrow from your bank, we may guarantee your mortgage so you can borrow after all( NOT A GOOD IDEA ). Everything that is desirable from a short-run Keynesian aggregate demand perspective (assuming these measures are indeed effective) is a step in the wrong direction from the perspective of restoring external equilibrium and raising the US national saving rate. ( THAT'S TRUE )

One obvious response to this opposition between what is desirable now and what is necessary in the longer run is to say: let’s do now what is desirable now and let’s take care of what is necessary tomorrow. That might be viable if the US private sector and the US policy makers had the necessary credibility to head south when the destination is north, because they can commit themselves to a timely reversal. If the authorities go ahead with the short-run Keynesian stimulus without having convinced the global capital markets and domestic producers and consumers that there will be a timely reversal, the policies will not work. ( TRUE )

This failure of expansionary fiscal policy is not for Ricardian reasons (Mr. Jean-Claude Trichet gets this wrong all the time - the Ricardian model has as one of its key assumptions that the government always satisfies its intertemporal budget constraint, that is, the government when it cuts taxes or raises spending today, is believed to raise taxes or cut spending by the same amount, in present discounted value, in the future; the second key assumption is that postponing taxes, while keeping their present discounted value constant, does not stimulate consumer demand. There either is no redistribution (from the young to the old, from those currently alive to the unborn and from those who are constrained by permanent income to those constrained by current income) or this redistribution does not have aggregate spending effects. Instead the failure of expansionary fiscal policy is because of the fear, uncertainty and higher risk premia ( TRUE )caused by the higher risk of sovereign default caused by expansionary policy.

If the government is believed to be fiscally continent (future taxes will be raised and/or future public spending will be cut by enough to safeguard the solvency of the state) but turns out not be so after all, the Keynesian fiscal policy will be effective in the short run (as long as the public believes in the fiscal virtue of the government) but will become highly contractionary once the truth dawns. ( TRUE )

Conclusion

Given the bad fiscal position of the US Federal government and given the vulnerability of the external position of the US and its growing reliance on foreign funding, the scope for expansionary fiscal policy in the US is much more limited than president-elect Obama’s advisers appear to realise. Underneath the effective demand problem is a deep structural rot, especially in household sector and financial sector balance sheets. Keynesian cyclical policy options that would be open to more structurally sound economies should therefore not be tried on anything like the same scale by the US authorities. "

I believe that the stimulus should not be more than:

Infrastructure: $100 Billion

Social Safety Net: Whatever is needed

Tax cuts: Sales Tax Cut and Targeted Investment Cuts: $300 Billion

Hopefully: $750 Billion

However, under my definition of stimulus, the figure is $400 Billion.

We should also make sure to keep repeating that we will in the future:

1 ) Raise taxes

2) Cut spending

3) Encourage saving

Finally, about the Saver Countries, I simply believe that it is going to be very hard for them to change.

{kind=link}

"Conclusion: if we can think of government investment projects that are productive, and give the government future income or give us future income, and which earn a good rate of return, this sort of government spending is not only good microeconomics, it can be good macroeconomics as well, if what you want is to increase aggregate demand."

This is true of any investment. The problem is that, even in the private world, there's no guarantee that money invested will be productive.

By the way, since government spends a large amount of our money, we must believe, or at least some of us, that some government spending is warranted.

In other words, neither the productivity argument or argument about whether government can do anything better is very useful here. Rather, in Debt-Deflation, we are trying any number of ways to get out of it. One way is to stop a savings spree that is part of debt-deflation. The question is can government spending stop a savings spree?

I say that it can, because it helps create a perception of investment and employment, as opposed to continual job losses and little or no new investment.My argument would be based on what people say about how they might react to a stimulus. That interests me more than theories, which assume behavior not in evidence. There are so many countefactuals being bandied about, it's hard to see them as anything but a list of possible cases, none of which might occur.